Fantasy or Foreboding? On Citrini's "2028 Global Intelligence Crisis"

Are the reactions to a flawed thought experiment more instructive than the predictions?

As a new piece of AI doomerism trends on X, I am reminded of Cunningham’s Law:

“The best way to get the right answer on the internet is not to ask a question; it's to post the wrong answer."

This time, Citrini Research has done us the great service of posting the wrong answer.

The piece, linked below in full, is a thought experiment in the form of a message from a future Macro Memo dated June 2028. To clearly quote the authors, it is “a scenario, not a prediction.” That said, it’s still a juicy piece of bait.

So what does their thought experiment actually predict?

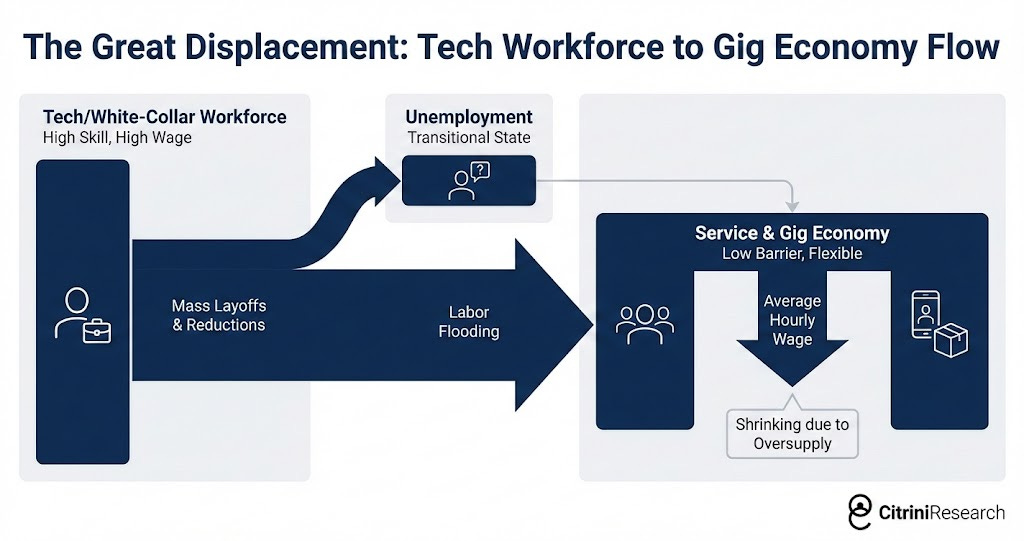

The core argument is that AI succeeding—not failing—is what breaks the global economy. That’s the "intelligence displacement spiral": AI improves, companies cut white-collar headcount, displaced workers spend less, consumer demand weakens, companies respond by investing more in AI to protect margins, which accelerates the next round of cuts. This is the underlying self-reinforcing loop.

LLM and agent usage will proliferate among the Late Majority of adopters to become the “default,” despite end users never understanding how they actually work (like web browsers or cloud computing). This means non-human agents become the dominant economic actors, unburdened by brand preference and unslowed by “habitual intermediation.”

Systemic risk will emerge from sector-specific risk as displaced workers reduce discretionary spending and downshift to lower-paying roles (compressing wages outside their original roles). This is accelerated and exacerbated by advancements in automation that disrupt the “gig economy.”

Finally, economic risks become fully realized when individual savings run out (unmasking the underlying weakness), debt and assets are “marked to market,” home values and mortgages implode, and the government becomes the ultimate backstop for human flourishing—the libertarian nightmare come true.

In all this gloom, there is at least one funny moment.

The “future” authors at Citrini note that despite the total collapse of white-collar work and cratering demand for humans that churn out memos, graphics, and PowerPoints:

“we are, somehow, still in business.”

No one is ever the victim in their own murder mystery. Citrini’s authors are just precog detectives, helping us identify the killers before they strike.

So are they right? Is this really how the economy will die? And if so, who’s currently holding the knife?

The Pushback Begins

It hasn’t taken long for the social internet to take Citrini’s bait. Between fawning reposts from bot accounts and amplification from the usual crop of AI doomers, the viral loop kicked in quickly on X. At time of publication, their original tweet has 20,000 likes and over 16 million impressions.

But, just as Cunningham’s Law predicts, the vocal critics arrived quickly.

John Loeber (who also publishes on Substack) posted “Contra Citrini7,” pointing out multiple weaknesses in the original piece. To summarize his points:

Citrini vastly underrates institutional momentum and inertia. Loeber cites the “iron rule” of human reality: “everything is always more complicated and takes much longer than you think it will, even if you already know about the iron rule.” This dampening effect is not taken seriously in the original piece, where it’s handwaved away by assuming artificial agents will take over for (and eliminate the friction of) human decision-makers.

Software companies aren’t lagging the market because of vibe coding; it’s because “an uncompetitive, sticky lock-in sector filled with dogshit incumbents is becoming competitive again.” That means there will still be a massive amount of interest in anyone (human or otherwise) that can handle the “last mile” of actually delivering a decent product to the end user. Loeber mentions the Jevons paradox, “when technological improvements that increase the efficiency of a resource’s use lead to a rise, rather than a fall, in total consumption of that resource.” Citrini and Loeber seem to disagree on the elasticity of demand for human labor and compute, as mediated by supply constraints (more on this to come).

Citrini isn’t considering that educated displaced workers would be absorbed by American re-industrialization. The US has a massive, politically bipartisan (read this as “fundable”) need to rebuild physical infrastructure and domestic manufacturing capacity—batteries, semiconductors, fertilizer, desalination, bridges. These projects are based in physical reality and inherently human-labor-intensive, and as such, they are not part of an imminent Singularity.

Whereas Citrini presumes the worst for the rate of worker displacement and margin collapse, they don’t presume the best for the strength of government intervention. Loeber notes that the federal government has shown it is capable of being “proactive and aggressive” when demanded by the markets. However, he stops short of identifying exactly when during the economic collapse this intervention would take place, nor which signals would be measured, nor whether by that time, AI agents will be running the government. (In this even, according to Citrini’s assumptions, we should assume a speedy, frictionless intervention via the direct distribution stablecoins, hopefully to humans!)

My oversimplification of Loeber’s points is:

“Citrini is overestimating the speed of disruption and underestimating the friction inherent in our economic system, beyond just the friction humans demonstrate in their decision-making and habit-forming.”

As this piece demonstrates, accepting or rejecting the Citrini hypothesis requires making multiple counter-assumptions both about the systems themselves and their inputs. It’s starting to sound like a physics problem:

How fast do these systems move under different conditions? How simple can our models of them be? How “closed” are these systems to external inputs? Does simply observing these systems change their potential behavior?

So: here’s another rebuttal authored by Michael Bloch of Quiet Capital, “THE 2028 GLOBAL INTELLIGENCE BOOM,” which mimics the form of the original post. He makes a different set of assumptions and reaches an opposite endpoint:

Citrini isn’t considering increasing consumer surplus as rent-seekers see their margins collapse. “The average American household was spending roughly $8,000–12,000 per year on services whose primary value proposition was navigating complexity on the consumer’s behalf.” Agents now return this value as available household spend. Bloch claims that technology-driven deflation has always expanded living standards, not contracted them, and this is categorically different from demand-driven deflation. Like Loeber, he uses a real estate analogy to show how buyers are keeping more of the value of their homes as commissions compress. (Loeber, in contrast, uses this as an example of something that won’t be disrupted quickly, thanks to the “iron rule.”)

Citrini is overstating the risk of financial contagion. Even if certain companies fail to pay their debts (Bloch cites Zendesk, so I’m guessing he’s not an investor), the damage will be contained. Booming productivity in other sectors would prevent loan portfolios from collapse, even as insurers took specific markdowns. Meanwhile, labor markets would only be temporarily impacted—perhaps AI agents are busy helping us all find our new jobs faster!—preventing a housing crisis from feeding into the feedback loop.

The government won’t need to overreact because the market will move faster than policy. Federal receipts might see a brief contraction, but they would recover thanks to corporate taxes and capital gains from a massive equity rally (“The S&P 500 crossed 12,000 last week. The Nasdaq is above 40,000.”) The “emergency” could resolve itself before legislation arrived.

Bloch insists that despite his fantastic projections for our collective economic triumph (such as the stock market doubling over the next two years):

This isn’t a libertarian parable. Public investment in retraining, community college modernization, and broadband infrastructure played a supporting role. But the primary adjustment mechanism was the market. Companies redeployed workers. Entrepreneurs started businesses. Consumers redirected savings. The feedback loop was positive, and it didn’t need the government to engineer it.

He claims a hypothetical senior product manager at Salesforce, rather than take a gig economy role after her layoff, would instead:

…[build] a niche AI-powered compliance tool for small healthcare practices, a market her former employer would never have served because the deal sizes were too small to justify the sales team. She had 200 paying customers within four months. Her revenue exceeded her former salary within eight.

He does not explain how she is outcompeting the other 500 product managers who were also laid off and decided to build the same tool, nor how the small healthcare practices avoided being demolished by the larger practices that were rolled up by AI-agent powered behemoths of private equity, nor how sustainable her revenue is when she is immediately disrupted by an autonomous Clawbot that clones her entire product in one query.

Pushing Back on the Pushback

Placing this obvious criticism aside, I’m making a larger point.

Disagreeing with Citrini’s thesis can take many forms. And when these disagreements occur, because the original thesis is still the locus of attention, we miss key tensions and conflicting assumptions between the counter-arguments.

Take these two rebuttals as examples. Loeber focuses on friction: institutions are stickier than models suggest, change takes longer than anyone expects, and that lag is protective. His arguments are anecdotal and he is skeptical of extreme outcomes. My interpretation is that his null hypothesis is: “Nothing Ever Happens.”

Meanwhile, Bloch focuses on flaws in the mechanism as described by Citrini. The model itself is wrong, regardless of the speed at which events unfold across its component systems. He makes structural claims about economic advancement, informed by centuries of technology-driven deflation improving living standards.

For Loeber’s projections to be correct, human behavior must be non-adpative, and institutional inertia needs to hold. Bloch’s projections rely on humans becoming more adaptive, like the laid-off product managers discovering their latent love of entrepreneurship.

Meanwhile, both authors fail to examine critical components of a deeply complex system. This is out of necessity, since they’re writing blogs, not books. But it’s still important to note what’s missing from both pieces: we can’t examine the assumptions held by the authors unless they’re made explicit, and we can’t trust predictions derived from incomplete models.

Here are just a few missing parts:

Geopolitical interdependence. What will happen to international labor markets, where the US and other developed nations have traditionally outsourced? What will be the policy response in those markets and from other developed nations? This is happening in real-time, not as a reaction to a potential localized recession.

Supply and capacity scaling for labor and compute. What is the impact of falling birth rates and immigration on local labor supply? How restricted will AI scaling be by the availability of compute and electricity? Will LLM performance continue to scale towards AGI, or will it be strictly constrained by its current design?

Second-order effects on social stability. Both pieces treat the market and the economy as the primary systems being measured and predicted, but this is not how most normal people construct their experience of the world. What happens to democratic institutions, social trust, and political legitimacy even under Bloch’s semi-utopian scenario?

Trust as economic infrastructure. Extending that, what happens to institutional and individual trust? It seems to break down in every subsystem referenced, and relied upon, by all these pieces. Why should we trust that AI agents routing around rent-extracting intermediaries will act in the consumer's interest? Why should displaced workers trust that they must retrain themselves for an AI-native world? Why should banks trust AI-native business models enough to lend against them? And in this brave new world—gulp—why should we trust the bloggers?

Clearly, Citrini’s piece has struck a nerve. But that’s not because it’s finely-tuned or particularly prescient.

Rather, it’s flawed in so many facets that it is inviting criticism from multiple angles simultaneously. This is always a brilliant strategy for going viral, since the internet can never resist sounding smart.

I’m not immune to this either. Hence, I’ve taken the bait.

But in reading this piece, I hope high-intent readers (bloggers, entrepreneurs, policy-makers) and low-intent readers (doomscrollers, AI summarization bots) will start to frame the assumptions, arguments. and counter-arguments about our hypothetical futures in more consistent terms.

Our exercise should not be in constructing the worst or best outcomes imaginable. Instead, we must reckon with the complexity of the systems we’ve built, our ability to observe and understand them, and the agency we have to make individual and collective choices that will shape them.

Otherwise, all we have are wrong answers.

Are We Cooked? is a public investigation into what’s actually happening with our technology, its new capabilities, and the consequences. Written and hosted by Tor Bair, it contains original writing, podcasts, guest interviews, and the occasional applied deep-dive. Learn more at: https://arewecookedhq.substack.com.

Good stuff